Juggling multiple debt payments each month strains your budget and your focus. Debt consolidation offers a structured path to manage this challenge. It combines several high-interest balances into a single new obligation. This strategy aims to reduce your overall interest rate. The result is a clearer, faster journey toward financial stability.

This approach simplifies a complex financial situation. You replace numerous due dates and payment amounts with one predictable payment. Debt consolidation can also lower the total cost of your debt. It creates a defined timeline for becoming debt-free. We will detail the specific advantages that accelerate your progress.

How Debt Consolidation Creates Financial Efficiency

The core mechanism of debt consolidation is straightforward. You acquire a new financial product to pay off existing debts. Common tools include a personal loan or a balance transfer credit card. This process merges your various payments. You then focus on repaying the single new account.

This method introduces efficiency into your financial life. It eliminates the confusion of managing multiple creditors. You gain a single interest rate and a monthly payment. This clarity is the first step toward faster financial relief. It transforms a scattered problem into a manageable plan.

The Direct Impact on Your Monthly Budget

Consolidation directly affects your cash flow. The primary goal is to secure a lower Annual Percentage Rate (APR). A lower rate reduces the interest portion of your payment. More of your payment then goes toward the principal balance. This accelerates your debt payoff timeline.

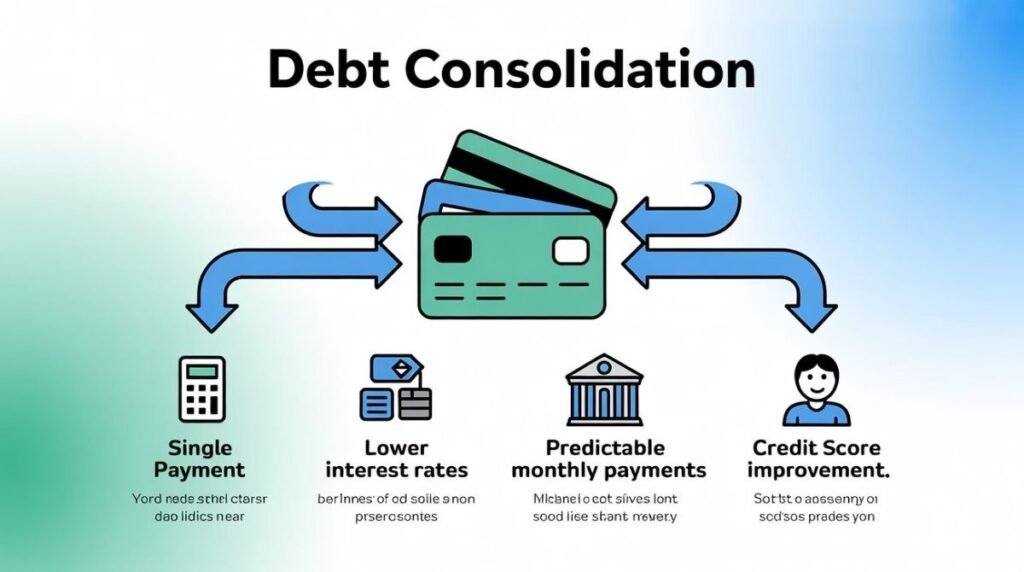

- Single Payment: Manage one due date instead of several.

- Lower Interest Cost: Reduce the total finance charges you pay.

- Fixed Payment Schedule: Know exactly when you will be debt-free.

Primary Advantages for Accelerated Payoff

The benefits of debt consolidation work together to speed up your financial goals. These advantages address common obstacles in debt repayment.

Simplified Money Management

Complexity often hinders financial progress. Tracking multiple bills increases the risk of a missed payment. Consolidation streamlines your obligations. You have one payment amount and one deadline. This simplification reduces stress and helps you stay organized.

Potential for Significant Interest Savings

High-interest debt, especially from credit cards, slows progress. A consolidation loan with a lower APR changes this. You pay less interest over the life of the debt. The table below shows a typical savings scenario.

| Debt Profile | Total Debt | Average APR | Monthly Payment | Time to Payoff | Total Interest |

|---|---|---|---|---|---|

| Before Consolidation | $20,000 | 22% | $506 | 5 years | $10,360 |

| After Consolidation | $20,000 | 12% | $445 | 5 years | $6,700 |

| Net Result | – | 10% less | $61 saved/month | Same Timeline | $3,660 saved |

A Clear Path to Debt Freedom

Seeing multiple balances can feel overwhelming. Consolidation provides a clear finish line. A debt consolidation loan has a fixed term. You know the exact date your debt will be zero. This tangible goal is a powerful motivator for staying on track.

Positive Credit Score Implications

Responsible consolidation can help your credit health. It lowers your credit utilization ratio when you pay off revolving accounts. Consistent on-time payments on the new loan build a positive payment history. These factors can lead to a higher FICO score over time.

Choosing the Right Debt Consolidation Method

Two primary methods exist for consolidating debt. Each has distinct features and ideal use cases.

1. Debt Consolidation Loan

An unsecured personal loan used to pay off other debts. These loans typically have fixed interest rates and set terms.

- Best for: Borrowers who want a fixed payment and a set payoff date.

- Look for: Loans with no origination fees and competitive rates.

2. Balance Transfer Credit Card

A card that offers a low or 0% introductory APR for a period. You transfer existing card balances to this new account.

- Best for: Those who can pay off the debt within the introductory period.

- Consider: Balance transfer fees and the standard APR after the promo ends.

Comparing Consolidation Options

This table outlines the key differences between the two main methods.

| Feature | Debt Consolidation Loan | Balance Transfer Card |

|---|---|---|

| Interest Rate | Fixed, based on creditworthiness | 0% intro APR, then variable rate |

| Repayment Term | 2 to 7 years | Must repay before promo period ends |

| Best Suited For | Structured, long-term payoff | Aggressive, short-term payoff |

| Impact on Credit | An installment loan lowers utilization | Installment loan lowers utilization |

Strategic Steps to Implement Debt Consolidation

A successful strategy requires careful planning. Follow these steps to ensure effective debt management.

- List All Debts: Note creditor, balance, APR, and minimum payment.

- Check Your Credit Score: Your score determines the rates you qualify for.

- Calculate Your DTI: Lenders review your debt-to-income ratio.

- Shop for Lenders: Get pre-qualified offers to compare rates and terms.

- Create a Post-Consolidation Budget: Allocate the money you save each month.

Avoiding Common Consolidation Mistakes

Consolidation is a tool, not a solution. Avoid these pitfalls to ensure long-term success.

- Accumulating New Debt: Do not use freed-up credit cards for new purchases.

- Extending the Repayment Term Too Long: A lower payment can cost more in total interest.

- Ignoring the Root Cause: Address spending habits that created the debt.

- Overlooking Fees: Factor in origination or balance transfer fees.

Who is an Ideal Candidate for Consolidation?

This strategy works best for individuals with specific financial profiles.

- Good Credit Score: Scores above 670 qualify for the best rates.

- Stable Income: You need consistent cash flow to make the new payment.

- High-Interest Debts: The strategy is most effective against credit card APRs.

- Financial Discipline: You must commit to not accumulating more debt.

Alternatives to Debt Consolidation

Consolidation is not the only path. Other options may better suit your situation.

- Debt Management Plan (DMP): A credit counseling agency negotiates lower rates on your behalf.

- Debt Settlement: Negotiating to pay a lump sum that is less than the full amount owed.

- DIY Snowball/Avalanche Method: Paying off debts strategically without a new loan.

[You can contact certified organizations like the National Foundation for Credit Counseling for professional guidance on repayment plans.]

Conclusion

Debt consolidation is a powerful tactic for achieving faster financial relief. It simplifies repayment and can reduce interest costs. The method creates a clear, structured path out of debt. Success depends on choosing the right tool and maintaining financial discipline. This approach can be the key to unlocking lasting financial freedom.

Frequently Asked Questions

Does debt consolidation hurt your credit score?

A small, temporary dip may occur after applying for a new loan. This is due to the hard credit inquiry. Over time, your score will likely improve. Factors include a lower credit utilization ratio and a consistent payment history.

Can I consolidate debt with bad credit?

Yes, but options are different. You may qualify for a loan with a higher interest rate. Some bad credit loan specialists focus on this market. A secured loan using collateral is another possibility.

How long does the debt consolidation process take?

The timeline can be relatively fast. Online applications take minutes. Approval may be instant or take a few days. Funding for a loan often happens within a week of approval.

Are there costs or fees associated with debt consolidation?

Yes, costs vary by method. Debt consolidation loans may have origination fees. Balance transfer cards often charge a fee for each transfer. Always read the terms carefully to understand all costs.

What is the difference between debt consolidation and bankruptcy?

Debt consolidation is a voluntary strategy to manage and repay your debts in full. Bankruptcy is a legal proceeding that can discharge some or all of your debts. Consolidation is a proactive financial tool, while bankruptcy is a last-resort legal option.