Managing overwhelming debt often feels like an impossible challenge. Effective debt relief provides a practical path forward. This process involves strategies to reduce or reorganize your obligations. The right approach can lower your monthly payments. It also creates a foundation for meaningful credit score improvement.

Rebuilding your credit requires a clear, actionable plan. Certain debt relief options directly address the factors that influence your score. These include your payment history and credit utilization. We will outline specific tips that connect debt reduction with credit health. This dual focus accelerates your journey to financial stability.

Understanding the Link Between Debt and Your Credit Score

Your FICO score is a numerical summary of your credit risk. It is based on the information in your credit report. High levels of debt negatively impact several key scoring factors. High credit card balances increase your credit utilization ratio. This ratio is second only to payment history in importance.

Debt relief strategies aim to reduce your outstanding balances. Successfully lowering these balances can improve your utilization percentage. This action often leads to a quick score increase. It also prevents further damage from missed payments or accounts going to collections.

How Credit Bureaus Calculate Your Score

Five main factors determine your credit score. Each has a different weight in the calculation.

- Payment History (35%): Your record of on-time payments.

- Amounts Owed (30%): Your total debt and credit utilization.

- Length of Credit History (15%): The age of your accounts.

- Credit Mix (10%): The variety of your credit accounts.

- New Credit (10%): Recent credit applications.

Proven Debt Relief Strategies for Credit Improvement

Not all debt relief methods affect your credit the same way. Some options are designed to protect your score during the process. Choosing the right strategy depends on your specific financial situation.

Debt Management Plans (DMPs)

A Debt Management Plan is a structured program facilitated by a non-profit credit counseling agency. The agency negotiates with your creditors on your behalf. They often secure lower interest rates and waived fees. You make one monthly payment to the agency, which then pays your creditors.

Credit Impact: A DMP itself is not directly reported to the credit bureaus. However, accounts included in the plan may be noted as “enrolled in a debt management program.” This notation is generally less harmful than late payments or collections. The primary benefit is that consistent, on-time payments through the DMP rebuild your payment history.

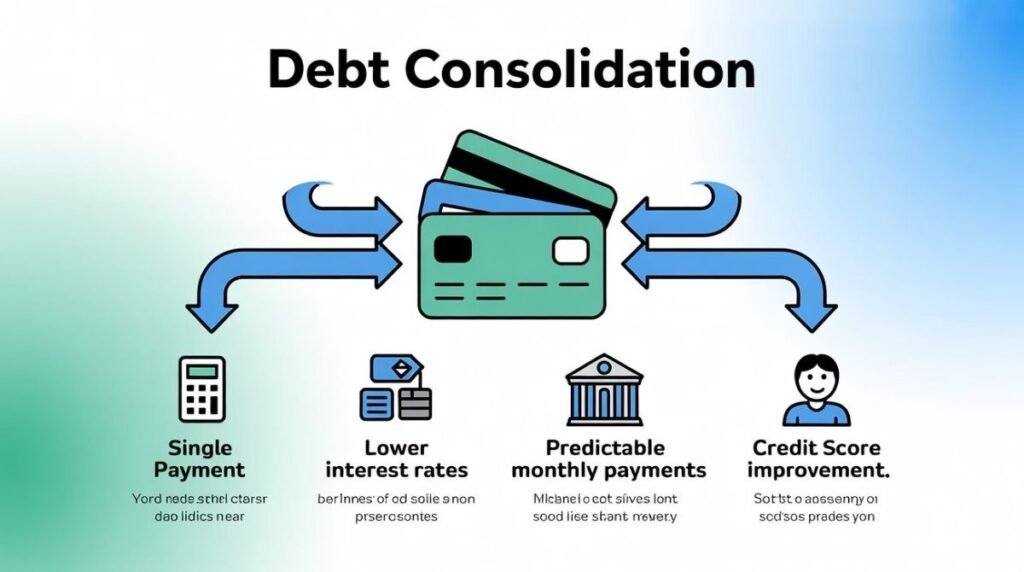

Debt Consolidation

This strategy involves taking out a new personal loan to pay off multiple existing debts. The goal is to simplify payments and secure a lower interest rate. This is a form of debt relief that focuses on reorganization.

Credit Impact: Debt consolidation can have a mixed effect. The initial hard inquiry may cause a small, temporary dip. However, paying off multiple credit card accounts will lower your overall credit utilization. This can result in a significant score boost. Success requires discipline to avoid accumulating new debt on the paid-off cards.

Debt Settlement

Debt settlement is a more aggressive form of debt relief. You or a company negotiates with creditors to pay a lump sum that is less than the full amount owed. The remaining balance is forgiven. This option is typically for accounts already in or near default.

Credit Impact: Debt settlement severely damages your credit score in the short term. Creditors will not settle until you are significantly behind on payments. These missed payments hurt your payment history. The settled account will be reported as “settled for less than the full amount,” which future lenders view negatively. The record remains on your credit report for seven years.

Comparing Debt Relief Strategies

This table outlines the core differences between the primary options.

| Strategy | How It Works | Best For | Typical Impact on Credit Score |

|---|---|---|---|

| Debt Management Plan | Counselor negotiates lower rates; you make one payment. | Those with steady income who can afford a reduced payment. | Neutral to Positive (rebuilds payment history) |

| Debt Consolidation | New loan pays off multiple debts into one payment. | Borrowers with good credit seeking lower interest. | Short-term dip, then Positive (lowers utilization) |

| Debt Settlement | Negotiate to pay a lump sum less than the full balance. | Those with severe hardship and no other options. | Significantly Negative (last resort option) |

[According to Experian, settled debts can remain on your credit report for up to seven years]

Immediate Actions to Protect and Improve Your Score

While pursuing a long-term debt relief strategy, you can take immediate steps. These actions help mitigate further damage and start the recovery process.

- Review Your Credit Reports: Get free reports from AnnualCreditReport.com. Dispute any inaccuracies immediately.

- Contact Your Creditors: Proactively explain your financial hardship. They may offer a temporary hardship program.

- Prioritize Minimum Payments: Avoid new late payments at all costs. Payment history is the most critical factor.

- Stop Using Credit Cards: Prevent your balances from increasing further.

- Create a Bare-Bones Budget: Identify every possible expense to cut. Redirect those funds to debt payments.

The Role of a Budget in Debt Relief

A realistic budget is the foundation of any successful debt relief plan. It provides a clear picture of your income and expenses. This clarity allows you to allocate maximum resources toward debt reduction. Use the 50/30/20 rule as a starting guideline: 50% for needs, 30% for wants, and 20% for debt and savings.

Rebuilding Your Credit After Debt Relief

Once you have addressed the debt, focus shifts to active credit rebuilding. Positive financial habits will gradually improve your score.

- Become an Authorized User: Ask a family member with good credit to add you to their account.

- Apply for a Secured Credit Card: These cards require a cash deposit as collateral. Use it sparingly and pay the balance in full each month.

- Consider a Credit-Builder Loan: The loan amount is held by the lender while you make payments. These payments are reported to the credit bureaus.

- Monitor Your Score: Use free services to track your progress and stay motivated.

Timeline for Credit Recovery

Recovery is a marathon, not a sprint. The table below provides a general timeline.

| Action | Immediate Impact (1-3 Months) | Short-Term Impact (6-12 Months) | Long-Term Impact (2+ Years) |

|---|---|---|---|

| Enroll in DMP | Stops late fees; accounts current. | Consistent payment history builds. | Significant score improvement likely. |

| Pay Off Cards via Consolidation | Score jumps due to lower utilization. | Score stabilizes at a higher level. | Positive if credit habits remain good. |

| Complete Debt Settlement | Score is very low. | Score begins a very slow climb. | Negative mark remains but impact lessens. |

Conclusion

Debt relief and credit improvement are deeply connected goals. A well-chosen strategy, like a Debt Management Plan or careful debt consolidation, can provide a direct path to a higher score. These methods address the root causes of credit damage. The key is consistent action and financial discipline. Reclaiming your credit health is an achievable milestone on the road to being debt-free.

Frequently Asked Questions

Will debt relief stop creditor calls?

Yes, most formal debt relief strategies can stop collection calls. Once you enroll in a DMP or retain a settlement company, creditors are typically notified. They will then communicate directly with your representative, providing you with relief from harassment.

How long does debt relief stay on my credit report?

The answer varies by strategy. A DPM notation may be removed once the plan is complete. Settled accounts and late payments associated with settlement remain for seven years from the original delinquency date. Positive information, like on-time payments, can also stay for up to ten years.

Can I do debt relief on my own?

Yes, a do-it-yourself approach is possible. You can contact creditors to negotiate lower interest rates or settlements. You can also create your own debt payoff plan. However, non-profit credit counseling agencies offer expert negotiation and structure, often at a low cost.

Is debt relief the same as bankruptcy?

No, they are distinct processes. Debt relief involves negotiating with creditors outside of court. Bankruptcy is a legal proceeding filed in federal court that discharges certain debts. Bankruptcy has a more severe and long-lasting impact on your credit report.

What is the best debt relief company?

Look for accredited non-profit agencies through the National Foundation for Credit Counseling (NFCC). Avoid companies that charge large upfront fees or make unrealistic promises. A reputable organization will offer a free consultation and clear explanations of all costs.