A home loan pre approval is your first serious step toward buying a house. This process evaluates your financial background and credit. It provides a clear picture of your borrowing power. A fast pre-approval gives you a competitive edge. You can make confident offers in a quick-moving market.

Speed depends on your preparation level. Organized applicants receive decisions faster. Understanding the lender’s requirements prevents unnecessary delays. We will outline the specific steps for a swift home loan pre approval. These tips streamline your path to a strong offer.

Understanding Pre-Approval vs. Pre-Qualification

Many buyers confuse these two terms. Knowing the difference is crucial for your strategy. A pre-qualification is a preliminary assessment. It is often based on unverified information you provide. This gives a rough estimate of what you might afford.

A home loan pre approval is much more rigorous. It involves a hard credit check and document verification. A lender underwriter reviews your complete financial profile. This process results in a conditional commitment for a specific loan amount. Sellers view a pre-approval as a sign of a serious, qualified buyer.

The Core Components of a Pre-Approval

Lenders focus on four key areas during their review. Strengthening these areas accelerates your timeline.

- Credit History and Score: Your credit score demonstrates repayment reliability.

- Income and Employment: Stable, verifiable income is a primary requirement.

- Assets and Reserves: You need funds for the down payment and closing costs.

- Debt-to-Income Ratio (DTI): This compares your monthly debts to your gross income.

Preparing Your Financial Documentation

Gathering documents before you apply is the single most important step. A complete package allows for immediate processing. You will need these core documents for a standard home loan pre approval.

Proof of Income

Lenders need to verify your earnings are stable. Provide your two most recent W-2 forms. Include your last thirty days of pay stubs. You will also need your last two years of federal tax returns. Self-employed borrowers need additional documentation like profit and loss statements.

Proof of Assets

You must show you have funds for the down payment and closing. Provide two months of statements for all financial accounts. This includes checking, savings, and investment accounts. Lenders will source these funds to prevent fraud.

Identification and Authorization

You need a valid government-issued photo ID. The lender will also require your signed permission. This allows them to pull your credit report from the three major bureaus.

Creating a Pre-Approval Document Checklist

Use this table to ensure you have every required item ready.

| Document Category | Specific Items Needed | Why It’s Important |

|---|---|---|

| Income Verification | 30 days of pay stubs, 2 years of W-2s, 2 years of tax returns | Verifies stable employment and gross income |

| Asset Verification | 2 months of bank/investment statements, gift letters (if applicable) | Confirms funds for down payment and closing costs |

| Credit & Identity | Social Security Number, Driver’s License/Passport, signed credit authorization | Allows for hard credit pull and identity verification |

| Additional Documents | Divorce decree, bankruptcy discharge papers, rental history | Explains specific financial situations or obligations |

Optimizing Your Financial Profile

A strong financial profile ensures a fast, smooth home loan pre approval. Address these areas several months before you start house hunting.

Check and Improve Your Credit Score

Order your credit reports from AnnualCreditReport.com. Dispute any inaccuracies immediately. Pay down credit card balances to lower your credit utilization. Avoid applying for new credit before or during the mortgage process.

Calculate and Lower Your DTI

Your debt-to-income ratio is a key metric for lenders. Calculate it by adding all monthly debt payments. Divide this by your gross monthly income. Most lenders prefer a DTI below 43% for a home loan pre approval. Paying down existing debt is the fastest way to improve your ratio.

Maintain Financial Stability

Do not change jobs during the pre-approval process. Avoid making large, undocumented deposits into your bank accounts. Consistency in your financial behavior reassures the lender’s underwriting team.

Choosing the Right Lender for Speed

All lenders offer pre-approvals, but their processes differ. Your choice impacts both speed and the strength of your pre approval letter.

Traditional Banks

These include national banks with physical branches. They may offer relationship discounts for existing customers. Their process can sometimes be slower due to larger bureaucracy.

Credit Unions

These member-owned institutions often provide personalized service. They may have more flexible underwriting for their members. Their rates can be very competitive.

Online Mortgage Lenders

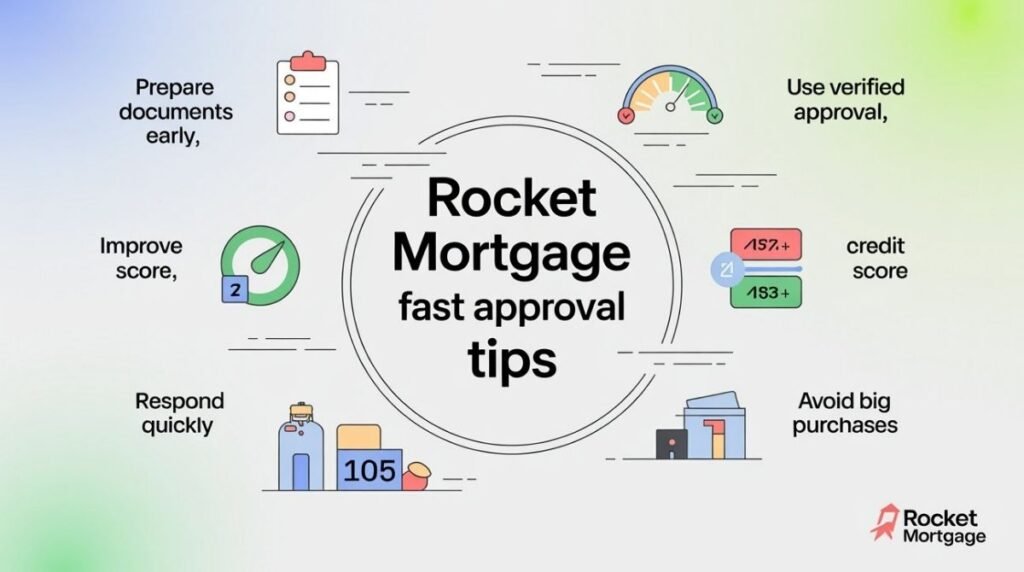

Companies like Rocket Mortgage operate entirely online. They often feature streamlined, fast application platforms. This can lead to quicker pre-approval decisions.

Mortgage Brokers

A broker shops your loan application to multiple wholesale lenders. This can help you find the best rate and program for your situation.

Comparing Lender Types for Pre-Approval

| Lender Type | Typical Speed | Technology Use | Potential for Personalized Service | Best For |

|---|---|---|---|---|

| Online Lender | Very Fast | High | Low | Tech-savvy borrowers seeking speed |

| Mortgage Broker | Fast | Medium | High | Borrowers who want multiple options |

| Credit Union | Medium | Medium | High | Members wanting a local relationship |

| Traditional Bank | Medium to Slow | Varies | Medium | Existing customers with complex finances |

Navigating the Application Process Efficiently

Your actions during the application directly influence the timeline. Follow these steps for a seamless experience.

- Get Your Documents Ready First: Do not apply until your document checklist is complete.

- Apply with One Lender Initially: Multiple hard credit checks in a short window count as one for your score.

- Respond to Requests Immediately: If the lender asks for more information, provide it the same day.

- Be Accurate and Consistent: Ensure all information matches your official documents exactly.

- Ask About the Timeline: Inquire about the average turnaround time for a pre-approval decision.

Understanding the Underwriting Review

An underwriter will verify every detail of your application. They confirm your employment and account balances. They analyze your credit history for red flags. Their goal is to ensure you represent a low lending risk. A clean, well-documented file passes through underwriting much faster.

The Power of Your Pre-Approval Letter

A strong pre approval letter demonstrates your financial credibility. It shows sellers you are a serious buyer. Your agent will likely include it with any offer you make. In a competitive market, this can make your offer stand out.

The letter typically states the maximum loan amount you qualify for. It may also include the type of loan, like conventional or FHA. Some buyers choose to get pre-approved for a higher amount than they plan to spend. This provides a buffer during negotiations.

Conclusion

A fast home loan pre approval hinges on your financial readiness. Organize your income, asset, and credit documents in advance. Choose a lender whose process aligns with your timeline and needs. Respond quickly to all requests for additional information. This proactive approach positions you as a powerful, prepared buyer in any market.

[Explore our latest guide on PenFed Mortgage Rates to compare loan options and find the best rates for your budget.]

Frequently Asked Questions

How long does a home loan pre-approval take?

With all your documents ready, the process can take as little as one to three business days. Delays happen if the lender must wait for you to provide missing paperwork or if your financial situation is complex.

Does a mortgage pre-approval hurt your credit score?

The hard inquiry from a single lender may cause a minor, temporary dip in your score. When shopping for the best rate, multiple inquiries within a 14-45 day window are typically counted as a single inquiry for scoring purposes.

How much does a pre-approval cost?

A legitimate home loan pre-approval from a reputable lender should not have an upfront fee. Be wary of any lender charging a significant fee just for the pre-approval process. Standard costs are typically limited to the credit report fee.

How long is a pre-approval letter valid?

A standard pre-approval letter is valid for 60 to 90 days. This is because your financial situation and credit can change. You can usually get an updated letter by confirming your information is still accurate with your lender.

Can a pre-approval be denied?

Yes, a pre-approval is a conditional commitment. A final loan approval can still be denied later if the property appraisal comes in low, your financial situation changes, or new red flags appear in the final underwriting.